Indian thermal coal imports

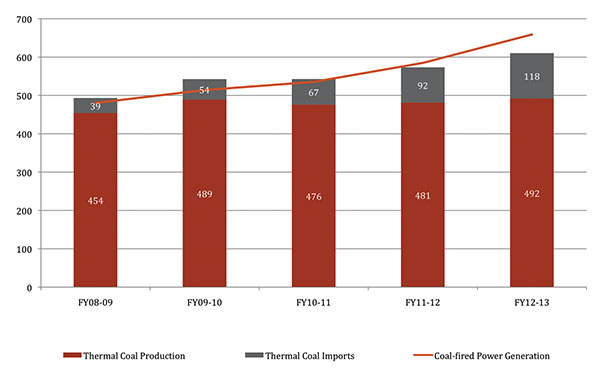

India is overtaking Japan as the second largest importer of thermal coal in the world, second only to China. India’s thermal coal imports grew at a staggering CAGR of 32% from 39 million t in 2008 – 09 to 118 million t in 2012 – 13. This growth in imports is primarily driven by demand from the power sector, which accounts for around 75% of the total thermal coal imports. However, thermal coal imports could have been greater if power tariffs had been more proportionate to changing dynamics in coal markets. With key tariff regulations beginning to change, Salva believes signs are moving in the right direction for import demand.

|

Figure 1. Indian power generation (TWh) and coal sourcing (million t). |

Power tariff regulations

Tariffs across power generation, transmission and distribution are generally regulated by Electricity Regulatory Commissions (ERCs). These commissions regulate tariffs for power companies, considering a government-specified return on equity. Alternately, power companies themselves bid certain tariffs for the life of a project or for a contract period.

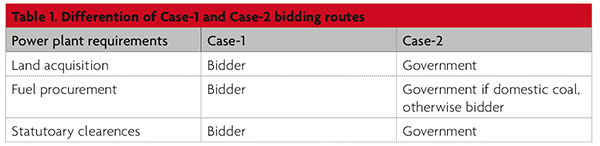

From January 2011, the Government of India necessitated all power generation projects be awarded based on a competitive bidding process, requiring developers to bid a lifetime tariff for a project.

As per the government’s competitive bidding guidelines, a power plant can be built through either Case-1 or Case-2 bidding routes, differentiated in Table 1.

The developer bidding the lowest tariff is selected and a power purchase agreement (PPA) is signed with the distribution companies. In both cases, the power plant developer can opt for either domestic or imported fuels or, alternatively, have them prescribed by the government.

Tariff structure

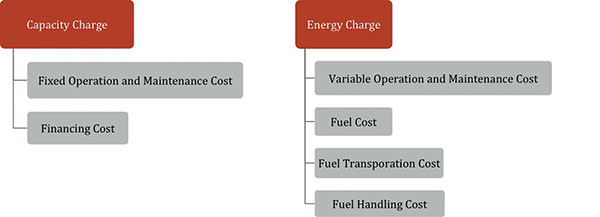

The tariff bid contains tariff components and escalation rates for the entire contract period, which is typically 25 years. The tariff bid is composed of several components:

- Capacity.

- Energy (fuel and non-fuel).

- Transportation and fuel handling charges.

These in turn all have scalable and non-scalable sub-components. Figure 2 demonstrates what capacity and energy charges broadly consist of.

| Figure 2. Capacity and energy charges broadly consist of the following. |

Scalable sub-components can increase bi-annually with certain escalation rates prescribed by the Central Electricity Regulatory Commission (CERC). However, bidders differentiate by quoting different ratios as scalable and non-scalable sub-components. A bidder quoting 100% of the increase in fuel costs as scalable will be able to pass through the complete fuel cost in the tariff.

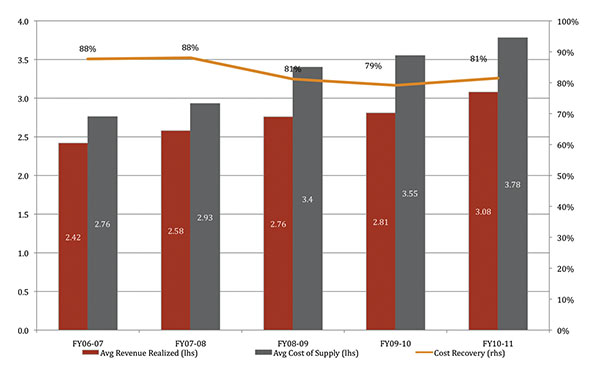

However, the ability of distribution companies to pass on the increased cost of power procurement to end customers is limited. This is due to some political compulsions (safeguarding political interests, while minimising subsidy burden on state governments) and, in some cases, the difficulty customers face in affording increased costs. The retail electricity tariffs are therefore not cost reflective and are heavily subsidised by the state governments. In such a situation, state distribution utilities – most of which are reeling from heavy financial losses as they have to absorb the increased cost of purchasing power – generally tend to restrain themselves from buying expensive power from the generators. Poor finance of distribution companies can lead to the risk of defaulting on or delaying payments to generators.

This lopsided nature of power tariffs restrains the ability of the power generators to import more coal, particularly of high gross calorific value.

| Figure 3. Gap between average cost of supply and average tariff (DNR/bwh %). |

Changes benefitting imports

Because a PPA is a binding agreement between the power supplier/bidder and thedistribution company, any increase in tariff is determined primarily by the percentage of scalable components and the escalation rates applied on them. In order to win a project, power producers tend to quote minimal scalable percentages, including that of fuel cost.

This trend, however, has proved unfeasible for many power projects, primarily ones based on imported coal. Imported coal-fired projects have recently faced several challenges, including sovereign policy change, currency devaluation and uncertain custom duties.

Due to sourcing problems in India, power generators such as Adani, Tata and Reliance bought coal mines in Indonesia. The expectation here was a cheaper source of coal. However, when Indonesia benchmarked its coal prices to international indices for all new and existing contracts, the cost of fuel procurement increased substantially. This significantly impaired the feasibility of long-term power supply contracts.

Many of the power plant developers bid low percentages for fuel cost escalation. The increase in fuel price could not be passed in the tariff to the required extent and resulted in financial losses to the generators. Both Adani and Tata now demand an increase in their power tariff, citing the increase in Indonesian coal prices. However, power procurers maintain that scope for such an increase should have been considered when bidding the percentages for scalable components in their power tariffs.

Policy changes and implications

In order to resolve these tariff issues, the government recently undertook certain policy initiatives.

Financial restructuring

In an attempt to improve the financial health of state distribution companies, the Ministry of Power (MoP) announced last year the financial restructuring of ailing state distribution companies (discoms).

According to the restructuring package:

- 50% of each discom’s short-term loans as of 31 March 2012 (which were mainly borrowed to bridge the gap between the price they pay to power generators and the price they receive from consumers) will be converted to bonds issued by discoms to lenders and guaranteed by state governments.

- Subsequently, the state governments will take over these bonds during next 2 – 5 years by issuing special securities to the lenders.

- For the remaining 50% of the short-term loans, the lenders will reschedule the loan and the discoms will receive a three year moratorium on principal repayments.

- The rescheduling of loans will be accompanied by initiatives focusing on increasing operational efficiency and timely tariff revisions.

To date, eight discoms have accepted this restructuring package and aligned with the initiatives. Some discoms have also moved ahead with tariff increases.

This move will push discoms to adopt regular tariff increases across all consumer categories (residential, commercial, industrial and agricultural), allowing gradual reduction in cross subsidy charge on industrial consumers. The periodic increase in discom tariffs will help them reduce their financial losses and enable them to purchase high priced power from generation companies. This will thus improve their payment clearance process to the generation companies. This process of tariff hikes will improve confidence of the generation companies in opting for increased imports of thermal coal, including better quality coal in lieu of poor quality domestic coal.

Compensatory tariff

In an unprecedented move, the Central Electricity Regulatory Commission (CERC) has mandated a variable compensatory tarrif to be offered to Adani’s Mundra thermal power plant and Tata’s Mundra ultra mega power plant (UMPP) to mitigate the standoff between increased fuel costs and rigid power tariffs. This will open the door to compensation for other power projects operating or planning to operate using imported coal but facing financial constraints.

This change will better enable the establishment of new power projects in scheduled time and improve power generation. This should result in an increased demand for imported coal in the absence of adequate domestic coal supply.

Custom duty changes

Aside from sovereign policy change, uncertain domestic policies, such as duties on coal imports, have also been a deterrent to coal imports. The government, in its union budget for 2012 - 13, announced 0% basic custom duty and 1% countervailing duty on steam coal imports. However, due to imprecise definition of steam coal (below 5831 kCal/kg) and bituminous coal (above 5831 kCal/kg), the majority of thermal coal imports attracted 5% basic customs duty and 6% countervailing duty as was applicable on bituminous coal. This imposition of higher duty on thermal coal imports increased fuel costs to several power producers, many of which could not pass through the cost in tariffs. However, in the union budget for the 2013/14 financial year, duties for both steam and bituminous coals have been simplified to 2% basic customs and 2% countervailing duty. This is also expected to boost imported thermal coal demand in India.

The future

With CERC’s consideration for an increase in tariffs, coupled with regular tariff increases, there is an indication that the Indian power sector is gradually moving out of its previously deadlocked situation. Additionally, the lessons learnt from aggressive bidding without considering future market risks will guide power plant developers to bid realistic tariffs in all future power plants. All these developments will result in cost reflective generation tariffs with increases in the purchasing and paying power of distribution companies, resulting in enhanced coal imports.

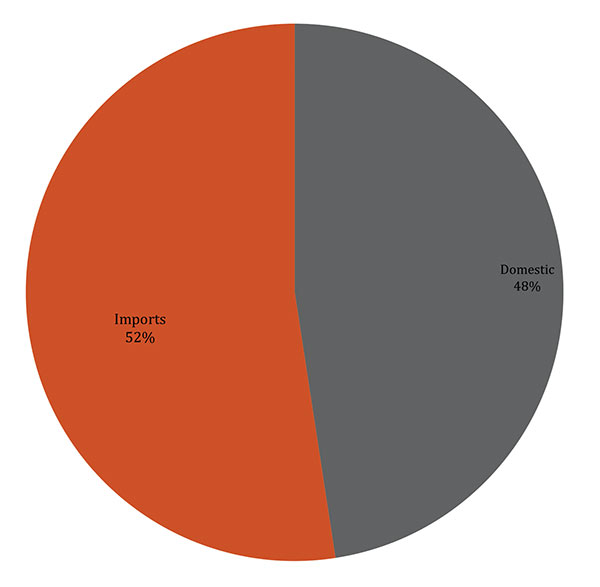

In the next five years, around 100 GW of new coal-fired power capacity is expected to be operational, which will create additional 350 million t of coal requirement.

| Figure 4. Power capacity addition and its coal demand in the next 5 years. |

However, domestic thermal coal production is expected to support merely 48% of this requirement, further growing India’s dependence on imported coal.

| Figure 5. Coal supply source for additional requirement. |

Mark Gresswell is director and chief analyst at Salva Report.

Read the article online at: https://www.oilfieldtechnology.com/special-reports/29072013/salva_report_india_power_tariff_regulations_and_thermal_coal_demand_285/

You might also like

Kongsberg Maritime selected by Samsung Heavy Industries for 9-ship Shuttle Tanker project for Tsakos Group

The vessels are being constructed for Greek shipowner Tsakos Group and will be a bare-boat charter by Brazilian energy logistics company Transpetro, supporting offshore operations in Brazil’s pre-salt oil fields.