India’s coal conundrum

India has a long history of commercial coal mining, dating back nearly 200 years. Coal mines were nationalised in the early 1970s in an attempt to meet the long-term coal demands of the country but also due to prevalent mining conditions, which included environmentally-damaging slaughter mining, the violation of mine safety laws, industrial unrest, the failure to make investments in mine development and an overall reluctance to mechanise the industry. Subsequent policy amendments have allowed captive mining to take place. This has enabled greater participation from the private sector, subject to the caveat that the mined coal is used in specific areas of the iron, steel and cement industries, power generation and coal-washeries. Although an initiative to increase private sector participation in coal mining was mooted through a bill that sought the denationalisation of the sector, it is still pending in the Indian Parliament. India boasts the world’s fifth largest coal reserves, yet it is still a net importer of coal.

Demand, supply and deficit

Coal sources

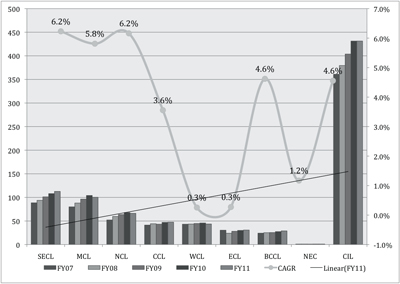

Coal India Ltd (CIL) and Singareni Collieries Co. Ltd (SCCL), two state-owned coal mining companies, dominate much of the domestic supply. Captive coal blocks allocated to end-users are the other major sources of supply. Domestic supply has been unable to keep up with the spurt in demand, leading to an ever-widening deficit in recent years.

Various challenges have hampered the growth of India’s domestic supply of coal. Some CIL mines have ceased production on account of technical problems, while others are awaiting forest clearance for their expansion. Some mines have suspended operations because it has become economically unviable to produce coal. Production from SCCL is also likely to remain stagnant.

CIL subsidiaries have a significant portion of underground mines that may not be able to add any further capacity. While some subsidiaries intend to increase capacity through opencast mines, overall contribution from these will be small on account of limited projects. A number of coalfields are also facing adverse stripping ratio. In the near future, Mahanadi Coalfields Ltd (MCL) is likely to contribute the highest proportion to the incremental production, since a large number of its projects are opencast greenfield projects. An analysis of key projects indicates that most of the incremental production is likely to come from high ash deposits, thus leading to a deterioration in overall calorific values.

Figure 1. Growth in coal supply (March 2012). Source: Ernst & Young.

Coal blocks allocated to end users may also add to the domestic supply as these consumers – power plants and steel producers – are going to make progress in the coming years. The author estimates the contribution of allocated captive coal blocks to overall domestic coal production will increase from the current levels of 5% to 15% by 2020. Overall, a growth in domestic supply of 5 – 6% CAGR is expected in the medium term.

Thermal coal demand

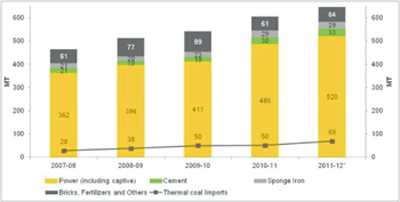

The power sector alone accounts for around 80% of thermal coal demand. The other non-power demand sectors are the cement, sponge iron (direct reduced iron) and brick manufacturing industries.

Figure 2. Thermal coal consumption and imports (March 2012). Source: Central Electricity Authority.

While economic growth in India has deteriorated over the last 18 months, addition to power generation capacity has not lagged, given the latent demand and the energy deficit that characterises the Indian economy. Several projects are in an advanced stage of construction and are likely to start production soon, thereby driving the demand for coal.

The trend has now shifted to creating large super-critical capacities around the coastal belt. This is likely to improve thermal efficiencies and reduce supply chain costs. Further, private sector participation in generation projects has increased three times during the 11th Five Year Plan (2007 – 2012). A large portion of projects were delayed during this period on account of EPC contracts, regulatory clearances and permits. An average delay of 17 months was reported in the projects over the plan period. Despite these factors, private sector participation in power generation is likely to outnumber both central and state government-sponsored projects, thereby commanding a major share in the wholesale markets.

Figure 3. Share in generation (March 2012). Source: Central Electricity Authority.

While renewable technologies such as wind and solar secure a significant portion of the investments in power sector, coal will remain a staple of India’s electricity mix. Looking at the power projects in advanced stages of project life cycle, various agencies estimate coal-fired thermal capacity addition to be around 200 GW by 2020. This may lead to a growth in coal demand of around 9% CAGR after adjusting for incremental thermal efficiencies offered by new technologies.

Figure 4. Yearly capacity addition (March 2012). Source: Central Electricity Authority.

Coal consumption across the cement, sponge iron and other sectors has grown by a CAGR of 10% during last five years. The future demand of all non-power end use industries will be strongly related to infrastructure development, which has become imperative to sustaining the economic growth that India has witnessed over the last decade. This fact has been well recognised by various governments, which have gradually increased infrastructure expenditure from US$ 24 billion in the 2002 financial year (5% of GDP) to US$ 83.5 billion in the 2010 financial year (7.2% of GDP). Going ahead, projects such as the dedicated freight corridor (DFC), the Delhi-Mumbai Industrial Corridor (DMIC), the development of various ports and the renewal of airports are expected to attract investment. Expenditure of 10% of GDP is targeted in the upcoming 12th Five Year Plan.

Factors such as increasing population, urbanisation, relaxation of floor space index (FSI) norms in cities and easier consumer financing options are likely to drive construction activities.

The sponge iron industry contributes about 5% to overall thermal coal demand and is inherently linked to growth of steel industry. It will continue to be coal-dominated in near future. While the crude steel capacity is expected to grow at a CAGR of 10.5%, growth in coal demand from sponge iron (coal-based) is expected to be around 7.5% CAGR on account of better efficiencies achieved through newer technologies.

The cement industry constitutes around 5% of thermal coal demand in the country. Coal is required for cement production and in captive power generation associated with the cement plants.

Figure 5. Demand sectors for cement.

In the 12th Five Year Plan period from 2012 – 2017, the planning commission estimates that the coal requirement for the cement industry will be in the range of 63 – 96 million t (46 – 70 million t for cement production and 18 – 27 million t for captive power).

Overall, coal demand from non-power end use industries is expected to grow at a CAGR of around 6% until 2020.

Policy action

The government recently began action to address the shortage of coal. After CIL missed the deadline to execute a fuel supply agreement (FSA) in March 2012, a presidential directive was sent to the company to complete it as soon as possible. Under the directive, CIL was asked to enter into FSAs with power companies, ensuring that it meets a minimum of 80% of coal requirement. While the power producers cheered the directive, they criticised key clauses of the new FSA proposed by CIL. The power producers have raised concerns about the review of the FSA after five years, wherein the seller has sole discretion over terminating the agreement, thereby implicitly limiting the term of the FSA to only five years. The rate of compensation for the “failed quantity” is also set too low as a penalty for non-fulfillment of obligations. CIL has now agreed to pay penalty of 1.5 – 40% on failing to supply the committed quantity of coal to the power producers, in the case of a supply shortfall below 80%.

In addition to the issues around assured quantities, power producers also want to address quality issues. There is a consensus that an auto-sampling arrangement should be made at all loading points and provisions be made for sampling at loading and unloading.

The board of CIL has approved the modified FSA with a “cost plus” model that provides imported coal at its actual cost. A plant load factor (PLF) of at least 80% would be assured through the FSA, with 65% met through domestic coal and 15% through imported coal. Newer producers have objected to this model, as their power production costs would turn out to be higher than that of existing players.

Lately, discussions on incorporating a price pooling mechanism have begun. Under this mechanism, all consumers of coal pay the same amount. This would result in rising coal prices, which in turn would mean higher costs for power. This move is likely to face resistance from existing power producers, who have not been able to pass on higher coal costs to consumers due to the possible political fallout. The model has been referred to the CEA and independent power producers (IIPs) for consultation. As this continues, many more views are likely to emerge in the area of pricing mechanism.

Meanwhile, last February the Ministry of Coal introduced the Auction by Competitive Bidding of Coal Mines Rule 2012. As per the rules, there are three processes to secure coal blocks for end use:

- Auction.

- Allocation to government companies.

- Allocation to power projects under tariff-based competitive bidding.

Under each of these mechanisms, the government will identify the area to be allocated to respective stakeholders. Under the auction route, which is for the non-power sector, it will earmark an area for each specified end use separately and notify a floor price. The government is currently working on the auction methodology and the determination of the floor price. For allocation to government companies, a separate area for each end use will be earmarked and a reserve price will be set. For allocation to power projects, the central government will earmark the area while the state government will select the bidders.

Outlook

The coal supply deficit, which stood at around 70 million t in 2012, is likely to increase substantially. There has been a drive to increase domestic supply and it is likely to rise by about 5 – 6%. However, demand is likely to increase at a much higher rate of about 8 – 9%. Resultantly, IPPs and end users will continue to scout for assets overseas and would look to increase blending. The blending constraints would restrict the quality specifications of the coal in the range of 4200 – 5200 kcal/kg (for sub-bituminous coal). To some extent, the level of imports will be constrained by government policies regarding the pricing mechanism. Further, an increase in import requirements is likely to put strain on port infrastructure, as well as impact trade deficit. It will also result in newer plants being installed close to the ports to reduce domestic logistics costs.

Written by Neel Kamal Goyal.

Read the article online at: https://www.oilfieldtechnology.com/special-reports/07022013/ernst_and_young_review_the_indian_coal_industry/

You might also like

How the US-Iran scenarios shape Brent prices

Rystad Energy has mapped a range of potential scenarios to assess their impact on oil prices, including the implications of continued disruption in the Gulf and a further escalation of conflict in the Bab el-Mandeb Strait.