Pipelines and control lines market update

Those with abundant reserves will strive to attract investment to enable adequate development to meet both domestic and foreign energy demands. As a consequence of these demands, we have seen growth in the offshore oil and gas industry since 2004. A lower price outlook and lack of available credit have questioned the future development of reserves, but growth in the industry is still expected to continue over the long term. Pipelines and control lines installation trends have mirrored those of the larger offshore industry, representing their crucial role within the offshore oil and gas infrastructure.

Predicting expenditure

Taken from their most recent industry model (Q209), Infield Energy Analysts forecast the total installed capital expenditure for pipelines and control lines to exceed US$ 241 billion over the 2009 to 2013 period. This equates to 71 103 km of lines being installed, of which 49 637 km will be pipelines and 21 465 km will be control lines. Combined, these represent an increase of 23% in installations on the previous five years.

Installation growth

New construction of pipelines will continue to push the technological boundaries of the industry as development of offshore O&G projects takes place across the world. The crucial role of bringing hydrocarbons to market means that new installation growth is expected in more countries, deeper waters and harsher environments; all of which challenges the industry in terms of material use and means of installation.

Keeping an eye on existing infrastructure

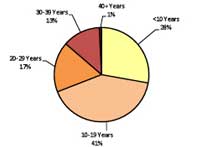

However, whilst new installations remain a key barometer for the health of the offshore industry, and thus receives significant attention, the age and integrity of some of the existing infrastructure is also becoming an increasing concern. For example, taking operational pipelines from the North Sea, we can see the extent of the issue. Currently, Infield has on record over 30 000 km of operational pipelines in the North Sea. Of these, over 72% have been operational for over 10 years. Most significantly, some 1% of these are over 40 years old and represent some of the key pipelines in the North Sea, notably the West Sole to Easington terminal and the Hewett- Leman-Bacton terminal lines.

The level of existing infrastructure in the UKCS acts as both a blessing and a curse. It makes the development of small fields through subsea tiebacks feasible through reducing the amount of CAPEX required. However, it also raises OPEX obligations, and as Figure 1 demonstrates, with 31% of existing pipeline over 20 years old, these obligations stand to be significant. The recent economic climate has resulted in many operators attempting to lower operating costs through improved cost efficiencies and as a consequence has seen the transfer of ownership away from major oil companies. However, a higher proportion of independents may face issues with the increasing maintenance costs and consequently could put their operations at possible risk.

figure 1: age of operational pipelines

figure 1: age of operational pipelines

The clock is ticking, if new projects are not developed soon the old export infrastructure may degrade to the extent that it will need to be expensively replaced, and so this presents clients with the option of ‘use it or lose it’ if they delay new projects for too long. In conclusion, both for new construction and maintenance of existing facilities the pipeline industry faces many challenges in being able to secure energy supplies from all offshore hydrocarbon basins, whether the new deepwater plays in West Africa and Brazil or managing the integrity of 30 - 40 year old pipelines that remain in operation in the North Sea and the Gulf of Mexico.

Author: Katy Simpson (Analyst) & Dr Roger Knight (Data Manager), Infield Energy Analysts.

Read the article online at: https://www.oilfieldtechnology.com/exploration/30092009/pipelines_and_control_lines_market_update/

You might also like

The operational realities of deepwater well testing

Reservoir performance specialist Ndubuisi Ezumba discusses with Contributing Author, Ellen Warren, how deepwater well-testing teams manage operational uncertainty, equipment reliability, real-time decision-making, and reservoir evaluation across complex offshore campaigns.