Time to step on the gas

Published by David Bizley,

Senior Editor

Oilfield Technology,

Joseph Gatdula, GlobalData, reveals the challenges that lay ahead for Egypt as it transitions from being a net exporter to importer.

The oil and gas industry in Egypt has experienced a rollercoaster ride in the last two decades, going from industry darling to regional laggard. Many of the factors that made Egypt a hotbed of investment have now been rendered ineffective due to short-term economic policies and the emergence of new exploration areas in the Eastern Mediterranean. Every mature oil and gas nation must face both the inevitable decline in production and a transformation from net exporter to importer, but how this transition occurs can influence its economic well-being for a generation. For Egypt, it will present multiple economic, political and social challenges.

Egyptian woes

Egypt’s oil and gas industry is undergoing a transition as dramatic as that experienced in its politics. Both have been fraught with missteps and errors but have since emerged from uncertainty to stability. With most oil and gas operations largely unaffected by the political and security instability experienced during the Arab Spring in 2011, the event gave both a cautious sense of change and reason to invest elsewhere. The resulting contested elections and ultimate military reorganisation gave pause to what was once Africa’s most prosperous nation. Still not completely clear of this political transition, Egypt is still literally paying for the lost years. Recent reports show the Egyptian government still owes around US$3.1 billion to its JV partners (mostly foreign companies), even after a December 2014 payment of US$2.1 billion. These payments are intended to alleviate the concerns faced by potential investors and reassure current operators. The delayed payments, which started before the Arab Spring, highlight the growing disparity between state revenue and debt commitments. The overthrow of President Mubarak increased economic pressure as exports slumped and investment fled. However, Egypt is facing a more considerable economic crisis as it transitions to a net importer of energy. Domestic gas subsidies (totalling US$26 billion in 2012) have distorted the market, with low price terms reducing investment viability in all energy projects.

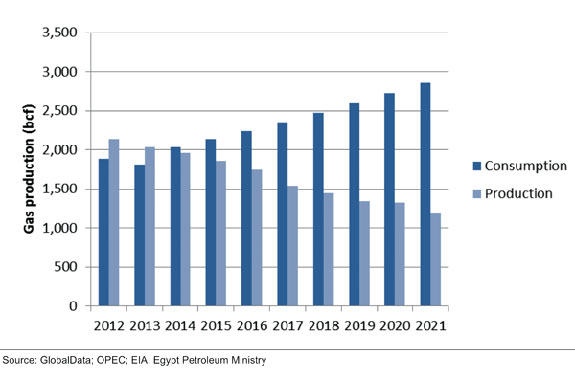

Figure 1. Estimated 10-year scenario (without a production improvement plan). Source: GlobalData; OPEC; EIA; Egypt Petroleum Ministry.

Government-mandated gas prices as low as US$2.72/1000 ft3 have ensured that demand stays high while disincentivising new investment or efficiency gains through conservation. In order to supply the domestic market with cheap gas, most production has now been diverted from export, causing Egypt to miss contractual export obligations and reduce state revenue. Egypt has become a net importer as the amount of gas required increases due to a combination of rising domestic demand and declining production. Weaning the country off artificially low gas prices will be a difficult transition for a restive population just recovering from a period of instability. Social and political ramifications of this transition will be a key test for the el-Sisi government, as this change will be the key to unlocking foreign investment and transitioning to a sustainable economic landscape.

Egypt’s bright spots

Egypt as a destination for oil and gas investment has multiple bright spots, which indicate that its recent decline may be premature. As a mature oil and gas region with first production in 1910, it currently ranks 16th globally in proven gas reserves with over 77 trillion ft3 of natural gas. The maturity lends itself to significant infrastructure, including several processing and export facilities in addition to LNG plants capable of exporting 7.2 million tpy.

Recent deepwater exploration and investment have proven successful and the prolific Western Desert continues to yield new discoveries and concession agreements. Recent bid rounds have been subscribed by a mix of oil majors and mid-sized independents with signed contracts of over US$2 billion of investment having been committed since late 2013. Cutting-edge projects are being executed throughout Egypt with a recent bid announcement for additional shale play areas near existing Shell and Apache shale projects. The DEKA Project came online in August 2014, providing a subsea production model for additional gas finds in the Mediterranean Sea.

Poor economics slow sanctioning of upstream gas projects

While Egypt accounted for 27% of Africa’s total natural gas production in 2013 with 2.03 trillion ft3, as of Q2, 2014 it is projected to produce 1.9 trillion ft3 for the full year. Production declines at gas fields come as domestic demand is rising and so new gas projects must be commissioned if Egypt is to meet this demand and avoid reliance on imports.

As part of efforts to tackle the gas supply deficit, the Egyptian government has indicated its willingness to collaborate with IOCs. The North Alexandria Concession was identified as a strategic project through which the country could address the impending supply issues. It is owned and operated by BP Egypt and LetterOne in a 60% and 40% partnership. Exploration began in 2000 and in 2010, the partners pledged to invest US$9 billion in development. However, the 2011 political crisis stalled proceedings until 2014, when representatives of BP and the Egyptian authorities signalled willingness to resume development.

In 2010, taking into account the project’s sizeable capital budget, the Egyptian government improved fiscal terms for the concession. This in addition to an increase in the agreed ceiling on domestic gas sales price from US$2.72/million ft3 to US$4.84/million ft3 has helped to assure investors. While these initiatives show the Egyptian authorities’ flexibility, these decisions were made over seven years ago and the previously agreed gas sales price will no longer support commercial development of the concession due to cost inflation. Given today’s current market conditions, more incentives must be granted to increase the viability of these marginal gas projects.

Figure 2. Fiscal regimes of the Eastern Mediterranean, base comparison results.

The domestic gas sales price is a major deterrent to most IOCs developing gas fields in Egypt. In November 2013, a government official confirmed that the gas sales price would be revised, with some rises taking effect in 2014 to US$8/million ft3 for the cement industry. GlobalData estimates the North Alexandria Concession to yield an Internal Rate of Return (IRR) of 10% and a payback period of over 25 years with its approved gas sales price of US$4.84/million ft3. This does not take into account the fact that required capital expenditure is likely to increase from initial estimates to between US$10 billion and US$12 billion, worsening valuation metrics. It is estimated that a revised gas sales price of US$6.50/million ft3 would yield an IRR of over 12% and reduce the payback period.

This is a typical investment decision scenario faced by most IOCs in Egypt, making it a challenge to sanction new gas projects. While Egypt has embarked on numerous short-term projects to import gas, such as the installation of floating storage and regasification units (FSRU) with a capacity of 170 000 m3, the North Alexandria Concession alone would add 800 million ft3/d during its peak, approximately 16% of the country’s total consumption of 2013.

The fiscal environment

The Egyptian fiscal environment has failed to adapt to the changing market dynamics in the region. A recent GlobalData fiscal study of regional regimes indicates that Egypt has fallen behind its peers in fiscal attractiveness. From the analysis, it was determined that IRR could be boosted for new fields by improving the cost recovery percentage and reducing the state take of production. These parameters are biddable items that companies can change based on the expected performance and investment performance expectations.

Based on the assessments, Egypt’s fiscal regime appears relatively unattractive. It also has one of the most restrictive commercial frameworks for natural gas. Egypt has stopped exporting gas and although domestic demand is strong, the standard pricing formula that EGAS uses for purchases of natural gas from operators sets a current price of around US$2.72/million ft3. Applying this price gives a negative NPV10 for all three test-field scenarios of 0.5 trillion ft3, 2.0 trillion ft3 and 7.0 trillion ft3. However, there are signs that the government is willing to negotiate with investors in order to facilitate investment decisions. In 2010, the government revised contracts with BP Plc and RWE Dea AG for the North Alexandria and West Mediterranean Deepwater concessions, allowing the West Nile Delta project to go ahead. Although the exact terms of the amendment were not released, it is thought to have altered both fiscal terms and the gas-pricing framework. GlobalData believes the government opted to implement a royalty and tax fiscal regime in contrast to the more traditional production-sharing contract.

This precedent may hearten those companies that were recently awarded exploration blocks in the deepwater Mediterranean bordering Cyprus in the current bidding round. It signals that while projects may not be commercially viable based on the standard PSA terms and domestic gas prices, flexibility in the government’s stance could render them profitable. However, the results of the above comparison between regimes in the region suggest that Egypt has a lot of ground to make up in order to render its fiscal terms competitive. Figure 2 shows the prices above which each field scenario yields a positive NPV10 for each regime. Given the difference between the regime’s break-even prices and Egypt’s current prices, an increase to make a project profitable could be difficult to attain and would probably still not make Egypt competitive in the region.

In order to make development of any ultra-deepwater gas discoveries commercially viable, Egypt may need to offer a combination of increased prices and eased fiscal terms. Although it appears that the requisite renegotiations were achieved for the West Nile Delta project in 2010, the prospects for similar flexibility on future projects appears more uncertain. The current authorities have expressed a willingness to renegotiate gas prices, but given the poor state of government finances, widespread changes to gas prices will be contingent on the current domestic price reform process for industrial and consumer supply. Moreover, the level flexibility on fiscal terms is more uncertain, particularly given that the current bidding round explicitly sets minimum bids and the West Nile Delta deal generated political opposition because of such changes. Furthermore, the level of flexibility may depend on the companies involved. BP has a long history of operations in Egypt and its existing relationship with the Ministry of Petroleum is likely to have eased negotiation, whereas other companies may not find the state so open to negotiations. Even if such flexibility might be possible, investors are likely to prefer opportunities that are inherently attractive, rather than commercial viability being contingent on the inherently uncertain outcomes of renegotiation.

As Egypt transitions to a net importer of gas, the challenge for the government will be to minimise the economic impacts of importing energy. The government will prioritise increasing production through increased foreign investment as well the transfer of technology and creation of jobs. To further facilitate foreign investment, Egypt must make structural changes to its domestic gas pricing, which currently hampers the viability of multiple projects and discourages investment. In addition, the large subsidies spent on energy imports decrease the funds available for social and economic development. Without pricing reform, Egypt will continue on an economic downward spiral with declining production and state revenue and increased trade imbalances due to more imported gas and higher net debt. If Egypt can successfully arrest the decline of domestic production through new foreign investment, it will see a two-fold benefit of decreased imports with additional state tax revenue. Allowing the market to determine domestic gas prices will be an unpopular fiscal policy in a country accustomed to low energy prices, but the difficult transition to net importer can be eased and even delayed while the economy shifts to a more stable and resilient model built on open-market pricing that encourages investment and reduces waste through conservation.

This article originally appeared in the February issue of Oilfield Technology.

Adapted for OilfieldTechnology.com by David Bizley

Read the article online at: https://www.oilfieldtechnology.com/drilling-and-production/10022015/time-to-step-on-the-gas/

You might also like

EnerMech completes complex offshore scope in Australia

EnerMech has successfully completed a complex offshore cleaning and preparation scope on the Bass Strait pipeline system in the Gippsland Basin, offshore south-east Australia.