Rystad Energy: ‘Trump 2.0. China 3.0 and OPEC+40’

Published by Elizabeth Corner,

Senior Editor

Oilfield Technology,

Rystad Energy: President Donald Trump’s potential second term, an anticipated decline in China’s oil demand and the forthcoming OPEC+ meeting are poised to shape the outlook for 2025.

Here is Rystad Energy’s oil market update from Global Head of Commodity Markets - Oil, Mukesh Sahdev:

"We're on the brink of major shifts in the oil market, driven by the potential return of a protectionist Trump 2.0 era and an outward-looking, expansionist China 3.0 moving beyond export-led growth.

These factors reflect an evolving approach – advancing into '2.0,' '3.0' and '4.0' iterations – updated versions that signal significant transformations ahead.

OPEC+ has evolved through three phases of market management with its emerging 4.0 policy focusing on price stability, crude market backwardation and the expansion of refining and petrochemical capacity both domestically and internationally.

As Trump 2.0 and China 3.0 take shape, OPEC+ is likely to proceed cautiously, extending production cuts for another one to two months with a strong focus on compliance, balancing crude exports vs. product exports, while closely monitoring ongoing conflicts in Russia-Ukraine, Gaza and Israel-Iran.

These factors will play a key role in shaping the events of the coming year and have the potential to significantly influence the outlook for 2025."

Brent oil futures have been hovering near US$70 – 75/bbl since the US election results in early November.

The Ukraine-Russia conflict is entering a new phase, with Ukraine launching long-range weapons to hit deeper into Russian territory, forcing Russia to elevate nuclear options.

The US veto of a UN resolution in a Gaza ceasefire has added additional geopolitical uncertainty and bullish sentiment.

The news of key Cabinet appointments in Trump 2.0 with a hawkish tariff-driven anti-China stance is adding a bearish bias.

Weekly builds in US crude and product inventories are providing another check on upward price movements.

The oil market is now bracing for OPEC+ action at the group’s 1 December meeting.

Looking ahead to OPEC+’s virtual meeting on 1 December, the group is expected to continue its cuts-compliance-quotas strategy to address the significant surplus on the crude supply side.

This surplus is driven by non-OPEC production growth and declining crude demand from refiners facing a bearish margins outlook.

The imbalance is even more pronounced in crude quality. OPEC+ has kept critical medium sour barrels off the market, while non-OPEC producers have added light sweet barrels (primarily from US shale) and medium sweet barrels (largely from Brazil).

The consensus on OPEC+ to further rollout the extension for cuts is strong.

However, the critical question is how long and is there a potential for surprise and signals for the emergence of a new OPEC 4.0 strategy?Outside OPEC+, the total US horizontal rig count further extended its downward trend, decreasing by three to 519.

Overall, the latest oil rig total stood at 449, relatively stable compared to a year ago, while the number for gas has declined by 21% to stand at 70 over the same period.

US commercial crude stocks increased by 5.81 million bbls in the week ended 4 October in line with seasonal builds and some impact of hurricane Milton on demand.

Non-OPEC+ supply growth: All eyes on the US

Non-OPEC+ supply growth in 2025 would be more than demand growth of about 1.1 million bpd, leaving little room for OPEC+ to unwind the cuts in place.

The year-on-year non-OEPC+ supply growth in crude and condensates is projected to be around 1.7 million bpd, whereas the total liquids growth is expected to be around 2.1 million bpd.

The Trump 2.0 rhetoric on increased drilling contrasts with the latest shale guidance striking a cautious tone on growth.

US total liquids growth is expected to touch 880 000 bpd, with 60% coming from the crude and condensate.

This is lower than the average growth of more than 1 million bpd pre-COVID-19 pandemic.

It is unlikely Trump 2.0 will achieve 20% growth in production as in Trump 1.0.

Even 10% is very ambitious and expected growth is less than 5%.

The 90% of non-US non-OPEC+ liquids growth of 1.3 million bpd is largely driven by Brazil, Canada, Norway and Argentina.

In a scenario where Trump 2.0 drives growth beyond the 1 million bpd mark, the price impact would certainly provide a check on the non-US non-OPEC growth as less than 10% of the growth will come from producing wells.

For now, it is realistic to conclude that the OPEC+ unwinding of barrels will certainly have a huge downward impact on the oil prices by around US$20/bbl and that is the only way to bring a check on non-OPEC+ growth.

The question is whether or not this is the strategy OPEC+ will pursue or will really want to take.

The answer to that question is very much dependent on the view of OPEC+ on oil demand growth and resulting crude demand growth. According to Rystad Energy’s analysis, the OPEC research group projected demand growth of 1.54 million bpd.

This is much lower than the group’s view in July this year of 1.85 million bpd growth.

The International Energy Agency (IEA), US Energy Information Administration (EIA) and Rystad Energy’s latest estimates for 2025 demand growth are 990 000, 1.22 million and 1.1 million bpd, respectively.

Thus, even with the higher side estimate of demand growth, it is not realistic to see a scenario of OPEC+ cuts full unwinding.

However, the OPEC research group has a much lower outlook of 1.1 million bpd of non-OPEC+ growth outlook, indicating that there is room to grow OPEC+ by 350 000 bpd only, which is much lower than 1.3 million bpd growth if the group executes the announced tapered unwinding of barrels.

If we look at the projected refinery crude demand growth of 900 000 bpd only, the opportunity to unwind crude cuts is even slimmer.

There is an increasing trend of refinery closures as well in 2025, which will exert further pressure on crude cut unwinding plans.

The conversation around China

With potentially aggressive or confrontational plans as part of President Donald Trump’s second regime to push significantly higher tariffs on China, the hopes of a China-led global demand recovery are fading.

For 2025, China demand growth is projected to be less than 100 000 bpd. China’s growth journey can be analysed in three stages:

- China 1.0: Growth driven by domestic consumption until the early 2000s. At that rate, China demand would have grown to only around 6 million bpd.

- China 2.0: As China started exporting and joined the World Trade Organisation (WTO), a significant demand growth surge occurred, with demand touching a level of 16.5 million bpd by 2023.

- China 3.0: This year has proved to be tough year for the Chinese economy, with growth stalling despite significant stimulus measures.

There are very strong and clear indicators for China establishing a manufacturing footprint in other countries to navigate the tariff-driven headwinds.

It is projected that China’s overall oil demand will peak by 2030 at 17.5 million bpd and the country may not remain the biggest buyer of crude oil.

Road sector demand has already passed its peak with accelerating penetration of electric vehicles (EV) and LNG trucks.

This is a key structural shift as China has learned that for moving vehicles it can use electricity, even if it is generated by fossil fuel.

This allows China to reduce its very high need for crude processing. China could still play a big role in the refined product exports market while utilising its refinery and petrochemical strength.

Uneconomic refining capacity is currently facing significant attrition in China, particularly with so-called ‘tea pot’ refineries and even a big refinery such as Dalian announcing closure (before relocation) amid changes in export tax rebates.

Therefore, China 3.0 is likely to be era of demand attrition domestically, driven both by Trump 2.0 tariffs and continued acceleration of the energy transition.

China 3.0 growth is more likely to come from the Chinese expansionist approach within Africa, Europe and Latin America, while Trump 2.0 follows an isolationist approach.

The Evolution of OPEC+ 4.0 and the roadmap for the year ahead

- OPEC+ 1.0: In the 1970s, OPEC countries began making significant production cuts, a response to the global oil shock that culminated in the 1973 oil crisis. During the 1980s, OPEC faced an oil glut, leading to several rounds of production cuts to maintain oil prices. However, in 1985, Saudi Arabia increased production sharply to punish non-compliant members, shifting the dynamics within the organisation.

- OPEC+ 2.0: By the early 2000s, OPEC nations ramped up production to meet rising global demand, reaching more than 45 million bpd. This period saw oil prices soar above US$100/bbl, boosting OPEC’s revenues. However, the US shale boom led to a market crash, and a price war ensued between OPEC and US shale producers.

- OPEC+ 3.0: The aftermath of the COVID-19 pandemic presented new challenges for OPEC, as the group struggled to return to pre-pandemic production levels amid a slower-than-expected demand recovery and rising output from non-OPEC countries. In response, OPEC+ implemented more than 5 million bpd in production cuts over several phases to stabilise prices. A distinctive feature of this strategy was targeting a backwardated market structure—where spot prices are higher than future prices—to discourage stockpiling and speculative trading. However, compliance issues arose, with countries like Iraq, Russia, and Kazakhstan consistently overproducing. Additionally, nations that adhered to the cuts often boosted product exports, sometimes exceeding pre-pandemic levels, which helped stabilise prices but also undermined the effectiveness of crude cuts.

- OPEC+ 4.0: As global demand recovery fades and geopolitical tensions rise – particularly with Trump 2.0’s proposed tariffs on China – OPEC+ faces limited options. The group has recently focused on enforcing stricter compliance with production cuts, especially from countries that have previously underperformed. While speculation about another price war to target US shale continues, the real concern is the pressure OPEC+ is putting on refinery margins. In response, OPEC+ members, particularly in the Middle East, have begun securing product market share by closing long-term crude supply deals in Asia-Pacific and expanding refining capacities, like the Fujian refinery in China and the Shaeen Petrochemical project in South Korea. Concurrently, refinery closures are accelerating globally, with China alone announcing the shutdown of 500 000 bpd of capacity. To balance the supply-demand equation, OPEC+ may need to cut product exports to stimulate crude demand from refineries worldwide.

Looking ahead, time beyond the new year holds a lot of uncertainty with this new OPEC 4.0 regime.

Higher compliance with agreed production cuts will be enforced to support oil prices.

However, short-term extensions of these cuts, lasting one to two months, are planned during the Trump administration's transition, which will help sustain backwardation in the market.

Pressure will remain on refinery margins to accelerate closures and secure a larger product market share for OPEC+ countries.

In mid-2025, crude production cuts may be reassessed in response to potential geopolitical events, such as additional Iranian sanctions, the escalating Russia-Ukraine conflict, or US-China trade negotiations.

OPEC+ will closely monitor the market to ensure price stability and preserve its influence.

Image: US liquids production outlook and possible Trump 2.0 impact.

Read the article online at: https://www.oilfieldtechnology.com/special-reports/25112024/rystad-energy-trump-20-china-30-and-opec40/

You might also like

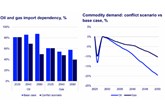

Middle East disruption could cut global oil demand 20% and gas 10% by 2050 as energy security drives shift to independence

Wood Mackenzie report that prolonged disruption to Middle East energy supplies could accelerate a structural shift in global energy systems, halving oil and gas import dependence by 2050 and reducing oil demand by 20% and gas demand by 10% relative to the base case.